What's behind Italy's economic turbulence?

Getty Images

Getty ImagesThe controversy surrounding the Italian government's spending plans has led to continued nervousness on the financial markets.

The budget set out by the country's coalition government last month - which involves greater spending than previously planned - had already sent Italian share prices lower and knocked the value of the euro.

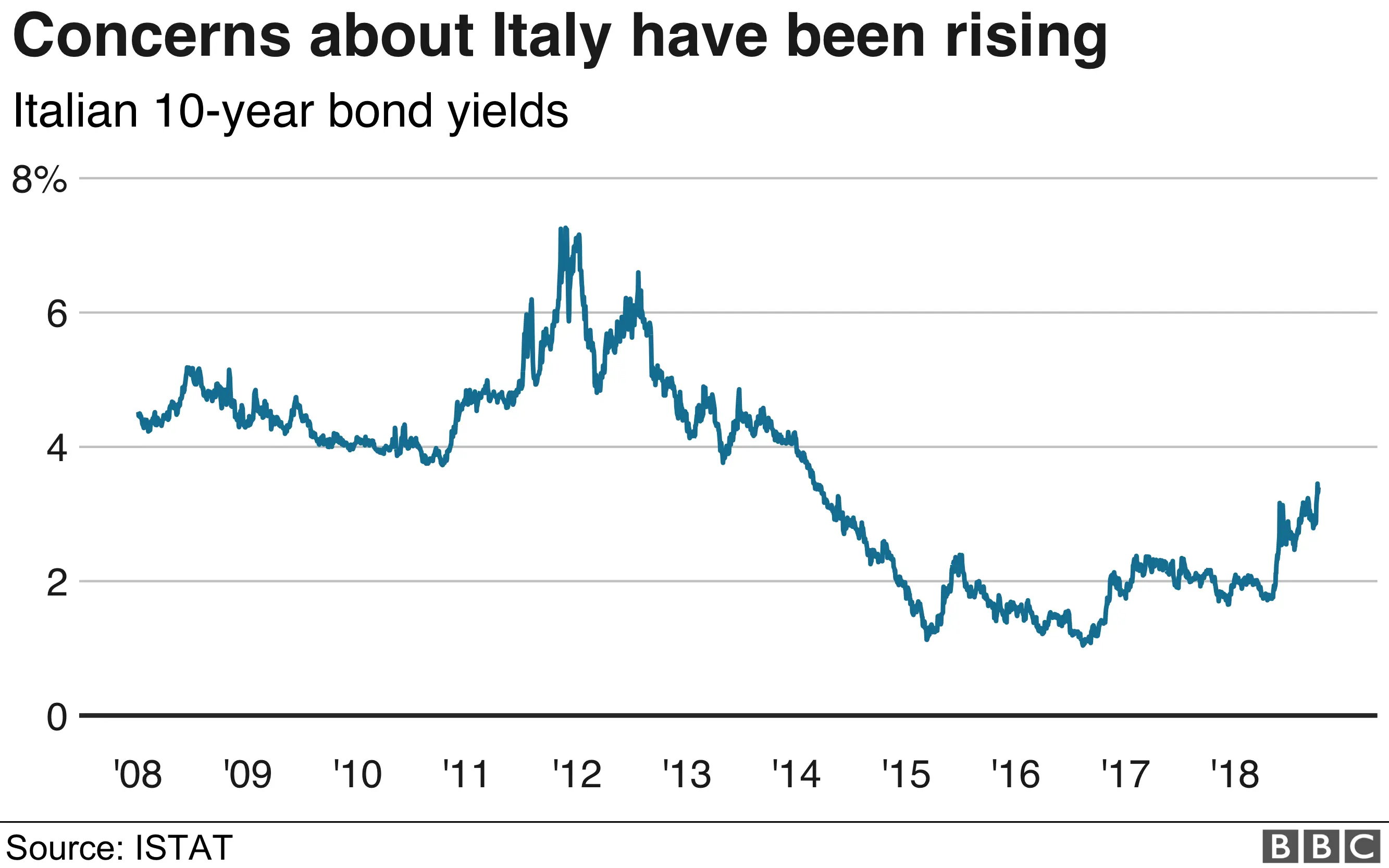

The cost of government borrowing for Italy, represented by the yield (or interest rate) on its bonds (the debt issued by the Italian government), has been rising, demonstrating that investors are getting twitchy.

Markets are concerned that the government's plans mean the country is heading for a stand-off with the European Commission.

Why is the Italian government's financial situation back in the news?

The government that took office after an election in March this year wants to be able to deliver on campaign spending promises. To do that it needs to borrow more than its predecessor was planning.

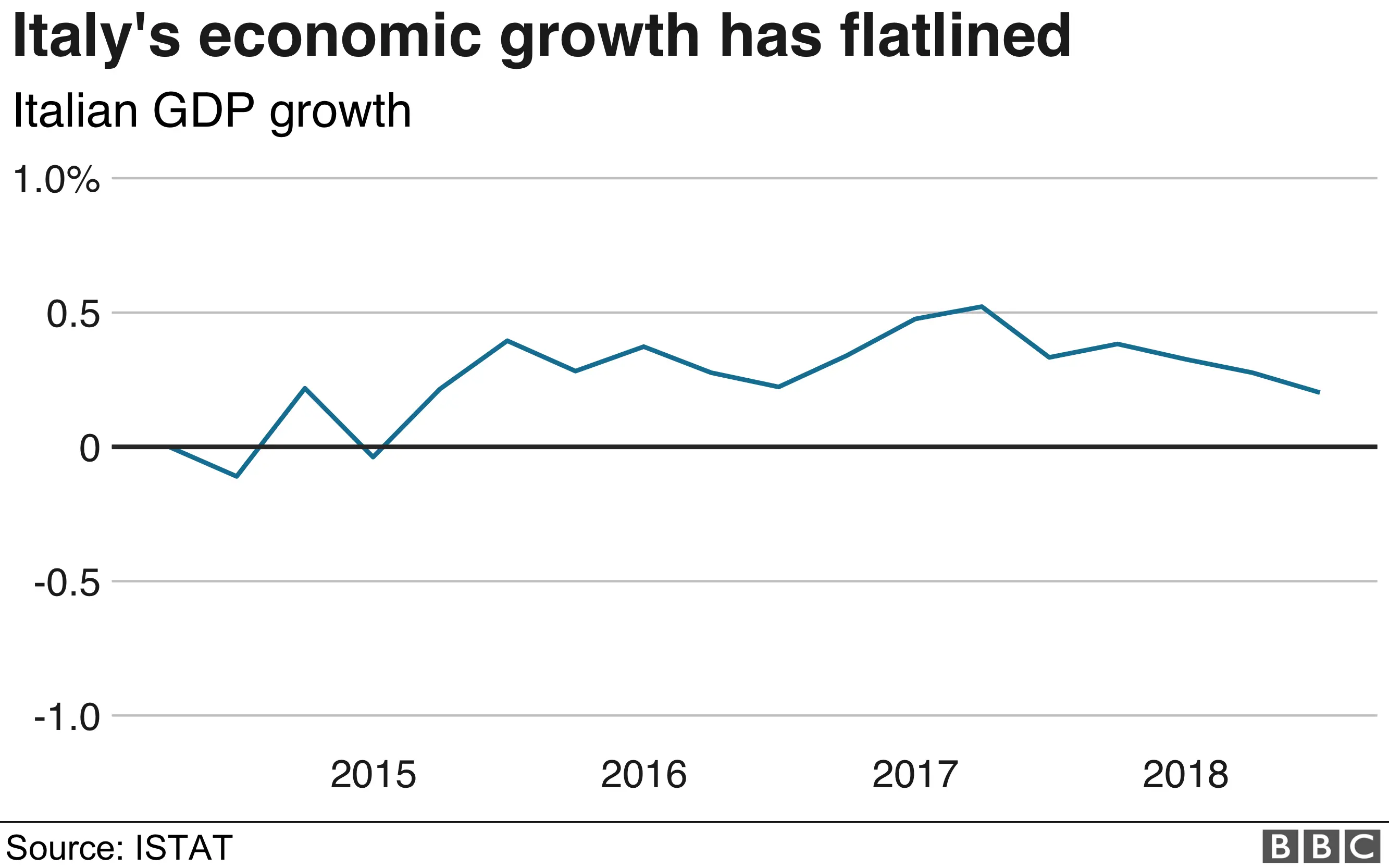

The government's ambitions to spend more are set against the sober backdrop of Italy's persistently weak economic growth record.

The determination to deliver on their election promises and that weak growth has once again raised questions about the sustainability of the country's debts.

There could also be legal action taken by the European Commission.

What exactly do they want to do?

The coalition government wants to reduce the retirement age, as well as increase spending on welfare and infrastructure. They want to finance it with more borrowing.

How much more?

The plan sent to the European Commission by the last government envisaged borrowing this year equivalent to 1.6% of annual national income (GDP), declining to 0.9% and 0.2% over the next two years.

That would be a budget that is very nearly in balance by the end of the decade.

The coalition is still wrangling over the figures for later years, but for 2019 they are aiming for 2.4%.

But isn't the upper limit for deficits under EU rules 3% of GDP? So what is the problem?

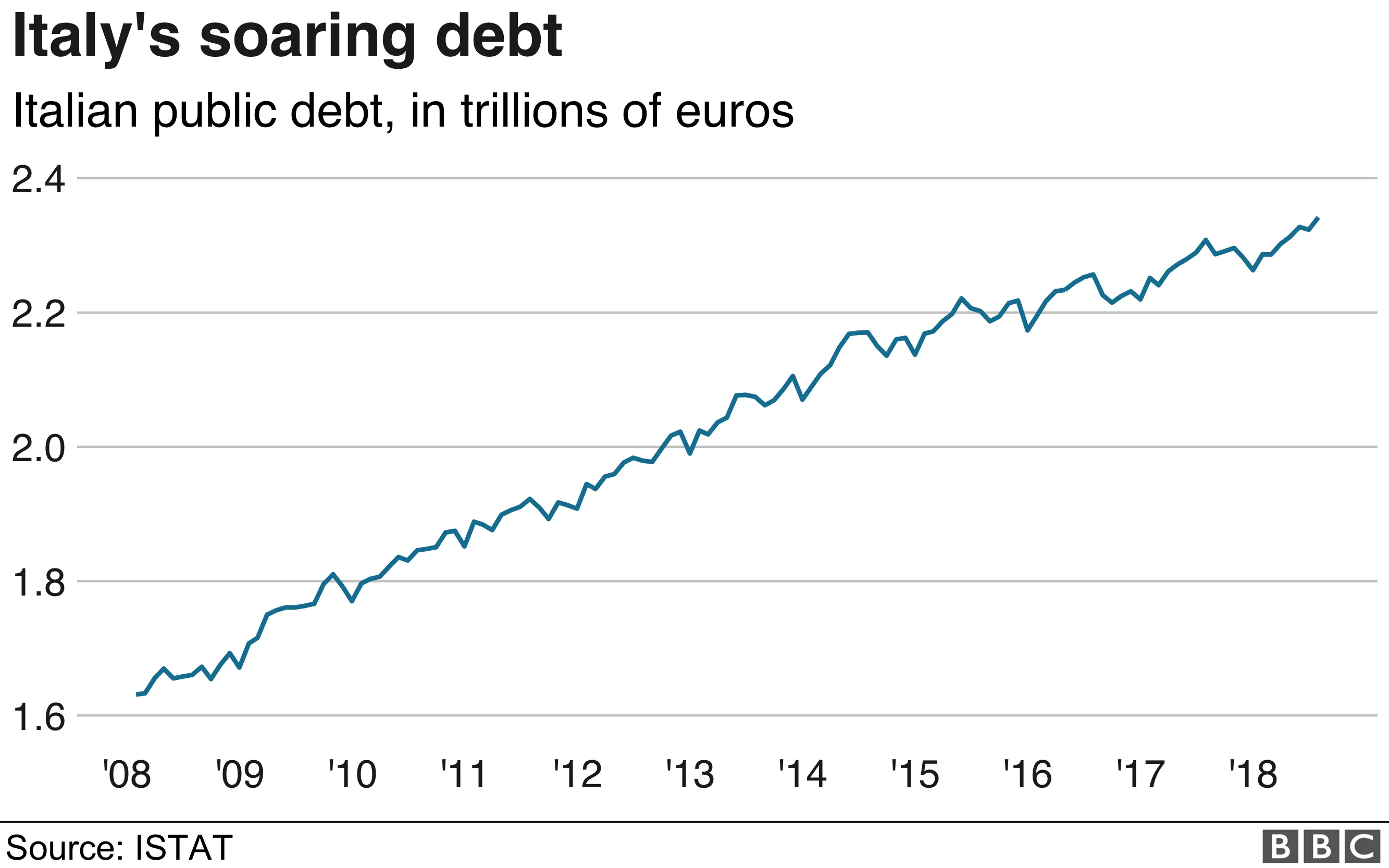

Yes, but there is another rule that total accumulated debt should be no more than 60% of GDP.

Italy has more than twice that amount. One way to get that total debt figure down is a lower deficit.

Couldn't Italy get the debt burden down with stronger economic growth?

In principle, yes. Stronger growth means GDP rises more rapidly so debt as a percentage of GDP declines. But Italy's problem has been one of persistently weak growth. The economy this year is slightly smaller than it was in 2005.

It is this growth problem that lies at the root of the strains on the government finances. Deficits were quite large in some years in the 2000s, but the figure has been 3% or less since 2012.

The debt burden has risen in the last few years because growth has been so weak.

How big is the debt?

In cash terms it's the biggest government debt in the EU at €2.3 trillion ($2.6tn; £2tn). The debt burden as a percentage of annual economic activity is second only to Greece in the EU at 132%.

What about the Italian banks?

Still a problem. Capital Economics, the London consultancy says the banks "remain the country's weakest link".

They own more than a quarter of Italian government debt, so they would be hit hard by a default. Even the rise in bond yields, which means the value of the bonds falls, is bad news for them. They also have high levels of problem loans.

The banks would also be vulnerable o renewed speculation that Italy might leave the eurozone. Deposits would almost certainly be pulled out of Italy in that situation as account holders wanted to avoid having their money converted into a new (or restored) national Italian currency.

That said, the Italian banks have a lot more capital than they did a few years ago which means they have more capacity to absorb losses. And the prospect of Italy quitting the euro has receded.

Have the financial markets been hit?

The starkest impact has been in the bond market, where the government's debt is traded.

The yields on those bonds give some idea of the government's likely future borrowing costs. They rose sharply in the past week.

The figures for Greece are higher, but Italian yields are markedly above the rest of the eurozone, including those countries such as Ireland and Spain that have had bailouts. There have also been impacts on the euro and the share prices of the country's banks.

What is the Armageddon scenario?

There are two. One is a default by the Italian government - a failure to repay debts as they come due. The other is leaving the euro.

Both possibilities were clearly in view at various stages with Greece. But the eurozone came through it. The size of the Italian economy and the government's debt burden mean that it would be much harder to deal with.

But neither is on the horizon with Italy. Although government borrowing is getting more expensive it is much cheaper than the levels seen as triggering the need for a bailout. Italy did get into that territory in the worst phase of the eurozone crisis, but is not close to that now.

There are people in Italy that want to leave the euro, and there is significant sympathy for the idea in the coalition parties. But it is not government policy.